Spring sun shines on the railways

Growth takes patronage to new record for the spring quarter

The pace of growth in demand for rail travel picked up in the spring sunshine, as passenger numbers were more than 7% up on the same quarter in 2024. The total including the Elizabeth Line reached a new all-time record for the April-June period, at 451.0 million. The previous record was set in 2019, at 435.2 million.

The pace of growth in demand for rail travel picked up in the spring sunshine, as passenger numbers were more than 7% up on the same quarter in 2024. The total including the Elizabeth Line reached a new all-time record for the April-June period, at 451.0 million. The previous record was set in 2019, at 435.2 million.

Overall, demand rose to 3.6% ahead of pre-Covid levels, according to National Rail Trends statistics, published by the Office of Rail and Road (ORR). However, without the Elizabeth Line, the recovery was limited to 91.8%. Even so, non Elizabeth Line passenger numbers were 7.3% higher than the same quarter in 2024, reaching another new post-Covid high.

The provisional figures cover the first quarter of fiscal year 2025/26, finishing at the end of June: across the network, 451.0m passenger journeys were made during the twelve-week period, up from 420.1m in 2024. Between them, they covered 17.1 billion passenger kilometres, 3.9% up, and paid a total of £3,100m in fares, 9.8% more than in 2024. This was the highest quarterly figure ever recorded.

Looking at demand by ticket type, advance tickets were up by 14.5%, taking sales 69.7% higher than before the pandemic. Anytime peak and off-peak tickets were up by 8.3 and 5.0% respectively, leaving them 21.7% and 37.7% ahead of the pre-Covid figure. Season ticket holders made 6.0% more journeys than last year, but the 55m total remained 61.2% below the 2019 figure.

Aside from the Elizabeth Line, services in London and South East moved ahead by 6.5% during the quarter, but this was once again the slowest growing sector. Between them, the operators carried 252.3m passengers in the twelve weeks, 12.4% below 2018/19. Amongst individual operators, West Midlands Trains saw the fastest growth on 12.9%, followed by c2c on 11.5% and Chiltern on 8.2%.

The Elizabeth Line carried 63.4m passengers in its twelfth full quarter of operation, 7.4% up in the year, meaning that the line accounted for 14.1% of the national network’s patronage in the April to June quarter, second only to GTR’s 17.3%.

The long-distance InterCity sector saw demand increase by 9.1% compared with 2024, taking passenger numbers to 38.5m, 6.4% above 2019 levels. The passenger kilometre figure was 5.1% ahead, leaving it 2.0% short of pre-pandemic levels. Revenue on the InterCity services moved up 7.9% (4.3% after inflation), but remained 15.6% down on 2018/19 in real terms. Cross Country saw the largest growth, on 15.2%, followed by LNER on 13.8%. Great Western grew by 8.2%, whilst EMR grew by 5.9%. Avanti West Coast saw 6.2% growth, whilst Caledonian Sleeper achieved 3.6%.

Amongst the regional franchises, total patronage was 9.0% up on 2024, coming to within 3.7% of 2019 levels. Amongst individual TOCs, Northern led the pack, with growth of 13.0%. Close behind came TransPennine, advancing by 12.9%, whilst TfW saw growth of 9.0%. Merseyrail’s patronage was up by 6.0%, whilst Scotrail saw a second successive increase of 2.2%.

Amongst the non-franchised operators, Arriva’s Grand Central operation reversed a previous fall, powering ahead by 12% in the quarter, 37.7% above 2018/19. Lumo also bounced back after a small fall, growing by 5.3 percent. Hull Trains saw growth of 3.3%, reaching 43.0% above pre-Covid levels. Competition from the Elizabeth Line still affected Heathrow Express. Patronage grew by 4.4% on the quarter, partially earlier declines. This left patronage on the premium route 28.4% down on 2018/19, despite record passenger levels at the airport itself.

Rolling year figures

The national totals for the twelve months ended 30 June show growth of 7.3% compared with 2023/24, 7.1% excluding the Elizabeth Line. Compared with the last pre-Covid year of 2018/19, the figure was just 0.2% lower at 1,759.5m. However, excluding the Elizabeth Line, passenger numbers remained 11.6% short of the 2018/19 figure. Passenger kilometres travelled were 7.2% higher at 64.2 billion, whilst passenger revenue grew by 10.9% to £11,503m. Adjusted for inflation, revenue was 8.0% up on the year, but remained 12.7% below pre-pandemic earnings.

As in previous quarters, performance varied between the sectors. Patronage on the InterCity routes was 9.1% up on the year, and moved past the 2018/19 total by 4.2%, despite a real terms shortfall in revenue of 16.9%. Regional networks saw growth of 9.0% on the year but remained 6.1% short of full recovery. Passenger journeys in London and South East excluding the Elizabeth Line saw the slowest growth at 6.2%, leaving the commuter lines 15.5% below 2019 levels.

Comment

Though the sun shone brightly, there were precious few reasons to be cheerful during the quarter, with Trump’s tariffs destabilising the world economy, a new war on the Middle East, and the increases in inflation as the increase in Employers’ NI took effect, and GDP growth slowed.

All of which makes the growth in rail patronage all the more remarkable. It was country-wide, too, with all TOCs recording an increase. Overall, franchised operations saw growth of 8.1%, TfL concessions 5.2% and open access 5.8%.

As in previous periods, the distinction between the TOCs that traditionally relied on commuters, such as Merseyrail and those in London and the South East, and the rest of the network is becoming clearer. There has been progress, though. During the quarter, only two operators remained more than 20% below their pre-pandemic patronage – Merseyrail (28.5%) and South Eastern (21.0%). Three others moved below the 20% line: South Western (18.8), c2c (18.5) and Chiltern (17.4). The only other operator to have a double-digit shortfall was Caledonian Sleeper (16.9%). Meanwhile, the Elizabeth Line continues to power ahead, growing by 8.3% during the year to 30 June, carrying a total of 247.6 million passengers, well ahead of forecast.

The contrast with the long distance market is stark. The sector was ahead of its 2018/19 patronage for the second successive quarter – mainly driven by the operators on the East Coast and Midland Main Lines, LNER and EMR. LNER maintained its impressive growth record with 13.8%, powering it a patronage figure no less than 30% ahead of its pre-Covid peak. The figures for the year also show growth of 13.0%, and a total 23.2% ahead of its previous high in 2018/19. Over on the Midland route to Sheffield and Nottingham, EMR’s quarterly growth was less spectacular, at 5.9%, but the total was more than 22.1% higher than the same quarter in 2019. The annual growth achieved was 8.6%, exceeding the annual pre-pandemic total by 20.8%.

The other long distance operators remained short of full recovery in 2024/25, Avanti West Coast by 10.4%, Cross Country by 4.3%, despite its impressive 15.4% growth in the year to 30 June. Great Western moved to within 8.9% – though the 2018/19 figure included a share of suburban traffic later transferred to the Elizabeth Line.

Once again, though, the problem remains revenue. The best example is the InterCity sector, where patronage might be more than four per cent above pre-Covid levels, but revenue remained 5.7% behind after adjustment for inflation.

Across the whole network, real revenue yields per passenger kilometre are 10.3% down, with all ticket types showing a decline, ranging from 12.1% on advance tickets to 3.9% on remaining season ticket sales. The position on advance tickets is particularly surprising given the flexibility to adjust these ticket prices in response to shifts in demand – of which there is no shortage, given the 73.5% increase in the number of passengers using them since 2018/19. This is surely one area where better yield management and greater commercial freedom could make a real difference; driving fares income up will be a key task for the new GBR management if their demands on the Treasury for subsidy are to be reduced.

Figures like these take us back to the days in the last decade when the railway was carrying more people than at any time since the early 1920s in the aftermath of the First World War. It all seems a long way from the dark days of 2020 and 2021. Long may it continue.

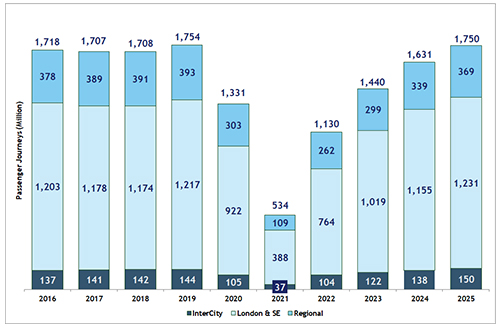

Passenger Demand by Sector for Year Ended 30 June

For more detailed analysis on these figures, you can view more articles about our analysis:

Quarterly Rail Stats - June 2025 gives our figures by sector for the quarter and the year, compared with 2024 and 2019.

Passenger Journeys by Operator - June 2025 shows the patronage for each TOC for y/e 31 March 2025, compared with 2024 and 2019.

This article also published in Rail Professional magazine