Summer sun shines on the rail market

InterCity and Regional Franchises see double digit gains, but revenue still falls short

Demand growth in the British rail industry accelerated again during the summer: non Elizabeth Line passenger numbers were 8.9 per cent higher than the same quarter in 2023. Including traffic on the recently opened line, growth was 9.1 per cent. Overall, demand rose to 97.2 per cent of pre-Covid levels, according to National Rail Trends statistics, published by the Office of Rail and Road (ORR). However, without the Elizabeth Line, the recovery was limited to 86.1 per cent.

Demand growth in the British rail industry accelerated again during the summer: non Elizabeth Line passenger numbers were 8.9 per cent higher than the same quarter in 2023. Including traffic on the recently opened line, growth was 9.1 per cent. Overall, demand rose to 97.2 per cent of pre-Covid levels, according to National Rail Trends statistics, published by the Office of Rail and Road (ORR). However, without the Elizabeth Line, the recovery was limited to 86.1 per cent.

The provisional figures cover the second quarter of fiscal year 2024/25, finishing at the end of September: across the network, 433.1m passenger journeys were made during the twelve-week period, up from 397.1m in 2023. Between them, they covered 16.7 billion passenger kilometres, 6.5 per cent up, and paid a total of £2,981.1m in fares, 13.1 per cent more than in 2023.

Looking at demand by ticket type, advance tickets were up by 17.3 per cent, taking sales 65.9 per cent higher than before the pandemic. Anytime peak and off-peak fares were up by 11.9 and 7.9 per cent respectively, leaving them 18.9 per cent and 23.3 per cent ahead of the pre-Covid figure. Season ticket holders made 0.3 per cent more journeys than last year, but the 49.9 million total remained 64.2 per cent below the 2019 figure.

Aside from the Elizabeth Line, services in London and South East moved ahead by 8.2 per cent during the quarter, but even so was the slowest growing sector. Between them, the operators carried 243.6m passengers in the twelve weeks, but remained 16.9 per cent below 2018/19. Amongst individual operators, Chiltern saw the fastest growth on 14.6 per cent, followed by West Midlands Trains (12.4 per cent) and South Western (11.8 per cent). London Overground saw the weakest growth at just 0.9 per cent.

The Elizabeth Line carried 61.0 million passengers in its ninth full quarter of operation, 10.2 per cent up in the year, meaning that the line accounted for 14.5 per cent of the national network’s patronage in the July to September quarter, second only to GTR’s 18.1 per cent.

The long-distance InterCity sector saw demand increase by 10.9 per cent compared with 2023, leaving passenger numbers just 1.5 per cent short of 2019 levels. Cross Country saw the largest growth, on 17.8 per cent, 6.6 per cent below pre-pandemic levels. EMR grew by 12.3 per cent, taking passenger numbers 22.0 per cent above pre-pandemic levels. GWR advanced by 11.7 per cent to 91.7 per cent of pre-Covid patronage, this comparison handicapped in part by the loss of Thames Valley suburban passengers to the Elizabeth Line since 2022. Avanti West Coast saw 11.5 per cent growth, still 8.0 per cent down from 2018/19. LNER saw the weakest growth, up by 6.7 per cent on the quarter, taking demand to 16.2 per cent above its 2018/19 numbers. The freshly nationalised Caledonian Sleeper operation saw a second successive fall, this time of two per cent, taking the business to 10.9 per cent short of previous highs.

Amongst the regional franchises, total patronage was 10.1 per cent up on 2023 but remained 12.9 per cent below 2019 levels. Amongst individual TOCs, TransPennine saw the strongest growth, with passenger numbers up by 25.3 per cent during the quarter, reducing the shortfall against their 2018/19 figure to just 0.9 per cent. TfW came next, advancing by 25.0 per cent, but still 18.8 per cent short of its 2019 figures. Northern saw a rise of 8.7 per cent in passenger journeys, leaving a shortfall of 9.8 per cent. Merseyrail saw growth of 5.5 per cent but demand remained 29.6 per cent down on 2018/19. Scotrail only managed a 0.6 per cent rise, even before the reimposition of peak fares last October, leaving it 12.9 per cent short of pre-Covid levels.

Amongst the non-franchised operators, First’s operations at Hull Trains and Lumo each saw double digit growth – 11 per cent at Hull Trains, taking patronage to over 54 per cent more than in 2018/19. Lumo achieved a hefty 20.3 per cent uplift. East Coast rivals Grand Central saw numbers fall back for the second successive quarter, but only by a barely perceptible 0.3 per cent, remaining 13.6 per cent ahead of their pre-Covid patronage. Competition from the Elizabeth Line drove patronage on Heathrow Express down for the third successive quarter, this time by 7.7 per cent. This left patronage on the premium route 35.2 per cent down on 2018/19.

Rolling year figures

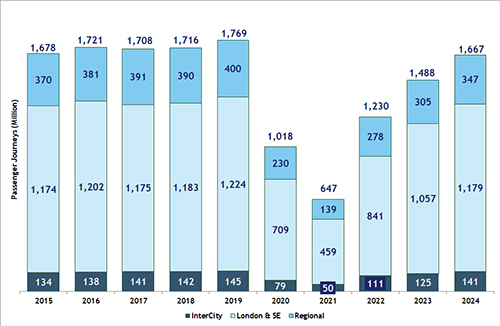

The national totals for the twelve months ended 30 September show that, compared with the last pre-Covid year of 2018/19, the number of passenger journeys was 5.7 per cent lower at 1,675.9 million. However, excluding the Elizabeth Line, passenger numbers remained 16.4 per cent short of the 2018/19 figure. Passenger kilometres travelled were 10.2 per cent lower at 61.2 billion, whilst passenger revenue saw a shortfall of 2.7 per cent at £10,242 million. However, adjusted for inflation, revenue was 17.9 per cent down on pre-pandemic earnings.

As in previous quarters, performance varied between the sectors. Passenger journeys were still 19.3 per cent below 2019 levels in London and South East and 13.2 per cent on the regional networks but moved to within 2.7 per cent on the InterCity routes.

Comment

This quarter saw the change of government after July’s general election, and an immediate change of pace on rail reform, with legislation rapidly tabled to exclude the private sector from train operation before the end of this Parliament. Meanwhile, robust growth was achieved by the “ancien regime” against a backdrop of faltering GDP growth and depressed consumer spending, as the country entered a prolonged period of limbo ahead of Chanceller Rachel Reeves’s October budget: as I’ve observed before, it is a backdrop that hardly presages a boom in demand for transport.

The rolling year patronage of total takes the network back to within 1.5% of patronage levels in the June-September quarter of 2018/19 – even if a hefty slice of the recovery is down to the Elizabeth Line. To the casual observer, this should mean that the crisis is over, shouldn’t it? After all, when we were at this sort of patronage levels in 2015, the government was making an £800m+ annual profit out of the passenger railway.

However, it is clear that, underneath the surface, shifts in the market have fundamentally changed the way customers use the network. As well as affecting the distribution of traffic across the working day and the days of the week, the changes have meant big shifts in revenue yields, so that the network is earning less money from the same number of passengers. At the same time, average journey lengths are shorter – 12.9 per cent lower in London and the South East and 7.9 per cent on the long distance InterCity routes.

Before the pandemic, season ticket holders accounted for 52.4 per cent of total demand on the railway. That’s 619m journeys covering 16.1 billion passenger kilometres (km), contributing £2,684m in revenue, giving a yield per passenger kilometre of 16.65p in the year to 30 September 2018. In the year to 30 September 2024, the season ticket market share had dropped to 218 million journeys, just 22.7 per cent of the total, covering 5.4 billion passenger km and earning revenue of £874m at 16.08p. That’s 67.4 per cent less revenue from 64.8 per cent fewer passengers, whilst earning 3.4 per cent less from each passenger kilometre travelled.

The number of anytime/peak ticketholders accounted for 36 per cent of passengers in 2018. That was 425 million, covering 12 billion passenger km, earning £3,765m at a yield of 31.39p. In the most recent period, the number of passengers had risen to 534 million, but only travelled for only 6.3% more passenger km, whilst the revenue had actually fallen to £3,441m at a yield of 27.00p. That’s 25 per cent more passengers but a revenue loss of 8.4 per cent and a yield reduction of 14 per cent.

Only two ticket categories show a real increase in revenue since the last pre-Covid year – advance purchase tickets and off-peak tickets. Advance purchases yield 13.01p, down by 10.8% from 14.59p. Passenger journeys by this ticket type have rocketed by 72.6 per cent, but the growth in passenger kilometres has been much lower at 25.8 per cent. Revenue, meanwhile, has only grown by 12.2 per cent. Sales of off-peak tickets show a similar pattern, with a 21 per cent increase in passengers, but just 9.5 per cent in passenger km. Revenue growth is restricted to 3.5 per cent, with yields 5.5 per cent lower at 16.26p.

The net result of all this is that, in the year to 30 September, the network carried 98.5 per cent of its pre-pandemic patronage, but only earned 82% of its real-term revenue. The bill for the resulting revenue shortfall of £2.3 billion lands of the desk of the Chancellor, alongside the cost of supporting Network Rail and the cost of HS2. That extra bill for the passenger railway might only be 1.3 per cent of the annual NHS budget, but it is nevertheless unwelcome in the current parlous state of the government’s finances.

One of the many questions facing DfT and the new GBR board is whether that shortfall can be made up from growth in revenue before the axe falls on service levels and investment. It may prove to be a close-run thing.

Also published in Rail Professional magazine.

Franchised Rail Passenger Journeys in Great Britain for the last 10 years, y/e 30 September

Additional information:

For the tables on the figures featured here: Quarterly Rail Stats - September 2024

Individual rolling year figures for each TOC: Passenger Journeys by Operator - September 2024