An autumn glow in the rail market

Annual long distance patronage moves to within one per cent of pre-Covid levels

Demand growth in the British rail industry slowed slightly during the autumn: non Elizabeth Line passenger numbers were 6.6 per cent higher than the same quarter in 2023, reaching another new post-Covid high. Including traffic on the recently opened line, growth was 6.9 per cent. Overall, demand rose to 97.1 per cent of pre-Covid levels, according to National Rail Trends statistics, published by the Office of Rail and Road (ORR). However, without the Elizabeth Line, the recovery was limited to 86.0 per cent.

Demand growth in the British rail industry slowed slightly during the autumn: non Elizabeth Line passenger numbers were 6.6 per cent higher than the same quarter in 2023, reaching another new post-Covid high. Including traffic on the recently opened line, growth was 6.9 per cent. Overall, demand rose to 97.1 per cent of pre-Covid levels, according to National Rail Trends statistics, published by the Office of Rail and Road (ORR). However, without the Elizabeth Line, the recovery was limited to 86.0 per cent.

The provisional figures cover the third quarter of fiscal year 2024/25, finishing at the end of December: across the network, 445.9m passenger journeys were made during the twelve-week period, up from 417.2m in 2023. Between them, they covered 16.2 billion passenger kilometres, 3.3 per cent up, and paid a total of £2,896.5m in fares, 10.7 per cent more than in 2023.

Looking at demand by ticket type, advance tickets were up by 13.3 per cent, taking sales 69.3 per cent higher than before the pandemic. Anytime peak and off-peak fares were up by 8.9 and 9.4 per cent respectively, leaving them 17.5 per cent and 26.2 per cent ahead of the pre-Covid figure. Season ticket holders made 3.6 per cent more journeys than last year, but the 60.1 million total remained 61.1 per cent below the 2019 figure.

Aside from the Elizabeth Line, services in London and South East moved ahead by 5.7 per cent during the quarter, but this was once again the slowest growing sector. Between them, the operators carried 247.5m passengers in the twelve weeks, but remained 17.5 per cent below 2018/19. Amongst individual operators, GTR saw the fastest growth on 7.0 per cent, followed by c2c on 5.4 per cent. West Midlands Trains saw a 2.8 per cent reduction during the period.

The Elizabeth Line carried 61.0 million passengers in its tenth full quarter of operation, 4.4 per cent up in the year, meaning that the line accounted for 14.5 per cent of the national network’s patronage in the October-December quarter, second only to GTR’s 18.1 per cent.

The long-distance InterCity sector saw demand increase by 8.7 per cent compared with 2023, leaving passenger numbers just 1.4 per cent short of 2019 levels. The passenger kilometre figure was 6.2 per cent ahead, leaving it 6.5 per cent short of pre-pandemic levels. Revenue on the InterCity services moved up 8.8 per cent (6.3 per cent after inflation), but remained 14.8 per cent down in real terms on 2018/19. LNER saw the largest growth, on 13.6 per cent, taking the business to 18.6 per cent above pre-Covid levels. The recently nationalised Caledonian Sleeper operation recovered somewhat after two successive falls in patronage, growing by 12.9 per cent, taking the business to 16.3 per cent above pre-pandemic levels. GWR advanced by 10.1 per cent to 91.9 per cent of pre-Covid patronage – though this comparison is still affected by the switch of suburban traffic to the Elizabeth Line since 2022. EMR grew by 5.5 per cent, taking passenger numbers 14.3 per cent above pre-pandemic. Avanti West Coast saw 4.4 per cent growth, still 13.0 per cent down from 2018/19.

Amongst the regional franchises, total patronage was 8.8 per cent up on 2023 but remained 11.3 per cent below 2019 levels. Amongst individual TOCs, TfW led the pack, advancing by 13.2 per cent, but still 8.7 per cent short of its 2019 figures. TransPennine came next, with passenger numbers up by 9.1 per cent during the quarter, reducing the shortfall against their 2018/19 figure to 7.7 per cent. Northern lost ground with a 0.4 per cent fall in passenger journeys, leaving a shortfall of 14.4 per cent. Merseyrail also lost passengers, with a fall of 1.3 per cent, taking demand down to 32 per cent below on 2018/19. Scotrail saw a 1.3 per cent rise, despite the reimposition of peak fares in October, leaving it 17.9 per cent short of pre-Covid levels.

Amongst the non-franchised operators, First’s operations at Hull Trains and Lumo each saw double digit growth – 19.3 per cent at Hull Trains, taking patronage to almost 95 per cent above 2018/19. Lumo achieved a hefty 23.0 per cent uplift. East Coast rivals Grand Central stabilised after two successive reductions, moving ahead by 2.1 per cent, now 24.9 per cent ahead of their pre-Covid patronage. Competition from the Elizabeth Line drove patronage on Heathrow Express down for the fourth successive quarter, this time by 13.2 per cent. This left patronage on the premium route 35.2 per cent down on 2018/19.

Rolling year figures

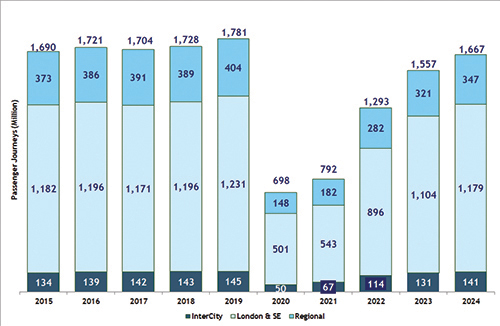

The national totals for the twelve months ended 31 December show that, compared with the last pre-Covid year of 2018/19, the number of passenger journeys was just 4.7 per cent lower at 1,704.8 million. However, excluding the Elizabeth Line, passenger numbers remained 15.2 per cent short of the 2018/19 figure. Passenger kilometres travelled were 9.0 per cent lower at 62.3 billion, whilst passenger revenue saw a shortfall of 0.9 per cent at £10,872 million. However, adjusted for inflation, revenue was 18.2 per cent down on pre-pandemic earnings.

As in previous quarters, performance varied between the sectors. Passenger journeys were still 18.1 per cent below 2019 levels in London and South East excluding the Elizabeth Line and 12.3 per cent on the regional networks but moved to within 0.8 per cent on the InterCity routes.

Comment

This quarter saw the new government’s long-awaited budget with its increases in taxation, alongside further moves to take the passenger railway back into public ownership. Lack lustre economic growth continued, with a fall in retail sales and an unemployment rate edging upwards. Another quarter in which the context for rail patronage was hardly encouraging. The quarter also saw a change of Transport Secretary as Louise Haig resigned over a past problem.

Despite this, the long, slow recover in patronage was maintained in all but three TOCs – two regional ones in Northern and Merseyrail and one hybrid, West Midlands Trains, which has a foot in both the regional and London commuter camps. All rely heavily on commuter movements, though Northern also continues to be plagued by reliability issues, particularly at weekends – increasingly amongst the busiest times on the network.

Merseyrail’s numbers are still almost a third down on pre-pandemic levels, the biggest remaining shortfall on the system. Five others are still over 20% down – Southeastern (26.4), c2c (25.3), Chiltern (24.5), South Western (24) and West Midlands (23.3). At the other end of the scale, there are now three TOCs and two open access operators carrying more passengers than in 2018/19 - LNER (18.6), Caledonian Sleeper (16.3) and East Midlands Railway (14.2). Amongst the open access operations, Hull Trains seem on course to double their pre-Covid numbers, having hit 94.9 per cent growth in the latest quarter, whilst Grand Central are 24.9 per cent higher. FirstGroup’s Lumo operation is of course a post-pandemic animal, but its 23 per cent growth in the quarter looks impressive. Whilst on the subject of non-franchised operations, the continuing decline of Heathrow Express is worth noting – double-digit decline in quarterly patronage has occurred in three of the last four quarters despite hefty and continuing growth in air passenger numbers. It’s clear that the service is never growing to recover its traffic, and one wonders how long its separate status – and occupation of scarce paths and Paddington platforms – can be maintained.

Whilst on the subject of open access operations, current attempts by FirstGroup, Virgin and Arriva (to name but three) to expand the sector seem to have alarmed the DfT. New informal guidance to ORR by the new Secretary of State Hilary Alexander in January asked the ORR to be “mindful of the impacts of Open Access such as the level of revenue they can abstract from contracted services and the associated implications for passengers and taxpayers”.

It is worth thinking more about that statement in the context of the current statistics. The total patronage of the four non-franchised operators was 2.25 million in the quarter and 8.99 million in the year. Ticket sales brought in £56.3m in the quarter and £237.7m in the year. The total quarterly patronage represented 0.52% of the national total and 1.9% of the revenue. The annual figures represented 0.53% of the patronage and 2.1% of the revenue. Not much to abstract there, really – especially if much of it would disappear if the services were forced to close. Even if the scale of open access operations were to double tomorrow, it would still represent something like one per cent of total demand and no more four per cent of revenue.

This suggests – to me at least – that the issue is not about abstraction, but about control. Success in generating new traffic for the network, high quality standards and high passenger satisfaction levels sacrificed on the altar of government or its agencies being in charge. This does not bode well for the role of private capital in investing in our economy, nor for the future of the rest of the network.

Passenger Journeys by Sector, Years Ended 31 December

Also published in Rail Professional magazine.

More details:

Quarterly Rail Stats - December 2024 for our presentation of the quarterly figures

Passenger Journeys by Operator - December 2024 - the figures for each train operator