Winter warmer from rail customers

Long distance patronage moves ahead of pre-Covid levels

Demand growth in the British rail industry slowed again during the winter: non Elizabeth Line passenger numbers were 5.6 per cent higher than the same quarter in 2024, reaching another new post-Covid high. Including traffic on the recently opened line, growth was 5.9 per cent. Overall, demand rose to 97.4 per cent of pre-Covid levels, according to National Rail Trends statistics, published by the Office of Rail and Road (ORR). However, without the Elizabeth Line, the recovery was limited to 86.5 per cent.

Demand growth in the British rail industry slowed again during the winter: non Elizabeth Line passenger numbers were 5.6 per cent higher than the same quarter in 2024, reaching another new post-Covid high. Including traffic on the recently opened line, growth was 5.9 per cent. Overall, demand rose to 97.4 per cent of pre-Covid levels, according to National Rail Trends statistics, published by the Office of Rail and Road (ORR). However, without the Elizabeth Line, the recovery was limited to 86.5 per cent.

The provisional figures cover the fourth quarter of fiscal year 2024/25, finishing at the end of March: across the network, 429.5m passenger journeys were made during the twelve-week period, up from 405.7m in 2023. Between them, they covered 15.8 billion passenger kilometres, 1.3 per cent up, and paid a total of £2,825.1m in fares, 9.5 per cent more than in 2024.

Looking at demand by ticket type, advance tickets were up by 13.6 per cent, taking sales 81.4 per cent higher than before the pandemic. Anytime peak and off-peak fares were up by 6.3 and 4.2 per cent respectively, leaving them 27.0 per cent and 32.0 per cent ahead of the pre-Covid figure. Season ticket holders made 5.6 per cent more journeys than last year, but the 60.1 million total remained 62.5 per cent below the 2019 figure.

Aside from the Elizabeth Line, services in London and South East moved ahead by 4.4 per cent during the quarter, but this was once again the slowest growing sector. Between them, the operators carried 240.3m passengers in the twelve weeks, but slipped back to 18.7 per cent below 2018/19. Amongst individual operators, West Midlands Trains saw the fastest growth on 9.8 per cent, followed by c2c on 7.2 per cent and Chiltern on 7.0 per cent.

The Elizabeth Line carried 59.6 million passengers in its eleventh full quarter of operation, 7.5 per cent up in the year, meaning that the line accounted for 13.9 per cent of the national network’s patronage in the January to March quarter, second only to GTR’s 17.8 per cent.

The long-distance InterCity sector saw demand increase by 7.7 per cent compared with 2024, taking passenger numbers to 36.9m, 3.7 per cent above 2019 levels. The passenger kilometre figure was 5.3 per cent ahead, leaving it 3.8 per cent short of pre-pandemic levels. Revenue on the InterCity services moved up 9.1 per cent (6.1 per cent after inflation), but remained 19.7 per cent down in real terms on 2018/19. LNER saw the largest growth, on 16.7 per cent, taking the business to 26.3 per cent above pre-Covid levels. Next came Cross Country on 14.3%, just 1.4 per cent short of 2018/19 levels. Great Western grew by 7.4 per cent, but remained 11.0 per cent short, whilst EMR grew by 6.7 per cent, taking passenger numbers 20.7 per cent above pre-pandemic levels. Avanti West Coast saw 2.3 per cent growth, still 13.7 per cent down from 2018/19. Caledonian Sleeper, though, saw a 5.2 per cent dip in demand.

Amongst the regional franchises, total patronage was 8.0 per cent up on 2024, but remained 6.3 per cent below 2019 levels. Amongst individual TOCs, TfW led the pack, advancing by 12.6 per cent, but still 4.7 per cent short of its 2019 figures. Northern bounced back from a drop in the last quarter to be 9.3 per cent up, remaining 7.3 per cent short of full recovery. TransPennine came next, with passenger numbers up by 8.5 per cent during the quarter, reducing the shortfall against their 2018/19 figure to 6.8 per cent. Merseyrail also bounced back from a loss in the autumn, with a rise of 7.7 per cent, taking demand to 25.2 per cent below on 2018/19. Scotrail saw a 2.2 per cent rise, despite the reimposition of peak fares in October, leaving it 14.6 per cent short of pre-Covid levels.

Amongst the non-franchised operators, First’s operations at Hull Trains saw growth of 8.7%, taking it to 44.8 per cent above pre-Covid levels, but Lumo experienced a small one per cent fall. East Coast rivals Grand Central also saw a small fall, of two per cent, but remained 12.7 per cent ahead of their pre-Covid patronage. Competition from the Elizabeth Line still affected Heathrow Express. Patronage grew by 4.4 per cent on the quarter, partially reversing five quarters of decline. This left patronage on the premium route 28.7 per cent down on 2018/19.

Rolling year figures

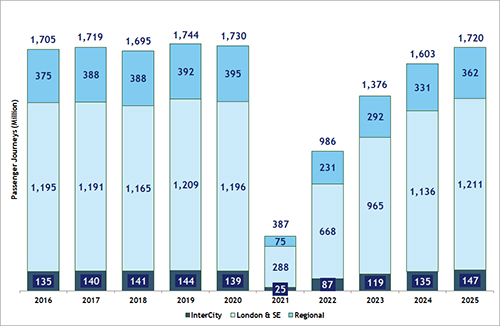

The national totals for the twelve months ended 31 March show growth of 7.2 per cent compared with 2023/24, 6.8 per cent excluding the Elizabeth Line. Compared with the last pre-Covid year of 2018/19, the figure was just 1.4 per cent lower at 1,728.7 million. However, excluding the Elizabeth Line, passenger numbers remained 12.7 per cent short of the 2018/19 figure. Passenger kilometres travelled were 7.5 per cent higher 63.0 billion, whilst passenger revenue grew by 11.1 per cent to £10,757 million. Adjusted for inflation, revenue was 4.8 per cent up on the year, but remained 16.4 per cent below pre-pandemic earnings.

As in previous quarters, performance varied between the sectors. Passenger journeys in London and South East excluding the Elizabeth Line were 6.7 per cent up on the year, but still 15.6 per cent below 2019 levels. Regional networks saw growth of 9.1 per cent on the year but remained 7.7 short of full recovery. Patronage on the InterCity routes was 8.4 per cent up on the year, and moved past the 2018/19 total by 2.3 per cent, despite a real terms shortfall in revenue of 19.6 per cent.

Comment

This quarter saw some measure of economic growth alongside falls in inflation and interest rates. It was also a relatively mild winter, with fewer severe weather incidents than some past years. A slightly more encouraging context for rail patronage with retail sales rising. All this was before the storms of the second quarter, with Trump tariffs, a new war on the Middle East and the increases in inflation.

The steady recovery in patronage was maintained in all the TOCs bar one, whilst there were also small falls in two open access operations – Caledonian Sleeper, Grand Central and Lumo. The winter quarter is the quietest time of the year, especially for leisure traffic, with demand typically dropping by two or three per cent compared with the autumn.

The distinction between the TOCs that traditionally relied on commuters, such as Merseyrail and those in London and the South East, and the rest of the network is becoming clearer. Five of these – Merseyrail, c2c, Chiltern, South Western and South Eastern – remain more than 20 per cent short of their pre-Covid patronage numbers. Meanwhile, the Elizabeth Line continues to power ahead, growing by 6.2 per cent during the year, carrying a total of 234 million passengers.

The contrast with the long distance market is stark. The sector passed the milestone of exceeding 2018/19 passenger journeys during both the quarter and the rolling year – though this is being driven by two operators on the East Coast and Midland Main Line routes, LNER and EMR. LNER’s growth of 16.7 per cent during the quarter was streaks ahead of the rest of the network, powering it a patronage figure no less than 26 per cent ahead of its pre-Covid peak. The figures for the year show growth of 10.2 per cent, and a total 19.5 per cent ahead of its previous high in 2018/19. Over on the Midland route to Sheffield and Nottingham, EMR’s quarterly growth was less spectacular, at 6.7%, but the total was more than a fifth higher than the same quarter in 2019. The annual growth achieved was 8.9 per cent, exceeding the pre-pandemic total by 17.9 per cent.

The other long distance operators remained short of full recovery in 2024/25, Avanti West Coast by 11.6 per cent, Cross Country by 7.0 per cent and Great Western by 11 per cent – though the latter comparison continues to be affected by the opening of the Elizabeth Line.

Looking at growth, mention must be made of the strong result achieved in Wales – helped by investment in new rolling stock, including the tram-trains and the electrification for the Valley Lines. The quarterly growth of 12.6 per cent contributed to an annual growth rate of 19.4 per cent. The annual figure is still 6.4 per cent short of 2018/19, but the trend is clearly in the right direction and represents a strong market response to the investment.

Once again, though, the problem remains revenue. The best example is the InterCity sector, where patronage might be above pre-Covid levels, but revenue most certainly isn’t, being 19.6 per cent behind in real terms.

Looking across the whole network, revenue yields per passenger kilometre are 9.3 per cent down overall, with all ticket types showing a decline, ranging from 12.9 per cent on advance tickets to 3.6 per cent on remaining season ticket sales. The position on advance tickets is particularly surprising given the flexibility to adjust these ticket prices in response to shifts in demand – of which there is no shortage, given the 78 per cent increase in the number of passengers using them since 2018/19. This is surely one area of freedom that should surely be restored to industry managers – a vital change in years to come if the demands on the Treasury for subsidy are to be reduced.

Meanwhile, credit is due to the management teams in both privately and publicly owned TOCs for the huge progress that has been made in recovering the industry’s market position from the dark days of 2020. Problems remain, but it is a huge achievement for which little credit is given by the media or politicians.

Annual Demand by Sector for the last Decade, years ended 31 March

For more detailed analysis on these figures, you can view more articles about our analysis:

Quarterly Rail Stats - March 2025 gives our figures by sector for the quarter and the year, compared with 2024 and 2019.

Passenger Journeys by Operator - March 2025 shows the patronage for each TOC for y/e 31 March 2025, compared with 2024 and 2019.

This article also published in Rail Professional magazine